PULSE Online Tool

PULSE, the IT support system for the Public Sector Accounting and Reporting Program (PULSAR), which supports the development of public sector accounting and financial reporting frameworks in line with international standards and good practices

PULSE Background

Provides a single tool to measure and report on both the conceptual and actual implementation of accrual accounting standards for the public sector according to IPSAS

Enables the identification of disconnects between the national and international PSA frameworks as well as the level of actual compliance with IPSAS based practices

PULSE Objectives

Support national and subnational governments in developing efficient and effective PSA systems.

Help public sector entities to develop an understanding of:

- Local PSA system and environment

- The gap between national and international PSA frameworks

- The gap in actual application between national PSA standards and IPSAS

Benefits of accrual basis PSA systems

Accountability

- Higher quality and improved reliability and comparability of the financial information.

- Enhanced political participation and inclusiveness.

- Improved trust in governments.

Transparency

- Complete picture of public finances.

- Better quality of financial information.

Financial management

- Improved basis for decision-making.

- Improved management of fiscal risks.

- Strengthened management and disclosure of assets and liabilities.

PULSE and PFM

An open and well-structured PFM which uses accrual basis IPSAS is one of the elements which helps achieve the three suggested budgetary objectives:

- Ensuring fiscal stability and the promotion of national economic growth

- Improving the acceptability and credibility of governments

- Improving and enhancing the quality of public services provided

PULSE and other assessment tools

PULSE was designed to complement other PFM assessment tools In particular, it is closely aligned to the following three diagnostic instruments:

- Report on the Enhancement of Public Financial Reporting (REPF). It should be noted that the PULSE methodology aims to replace the REPF

- PEFA. The PULSE framework was designed to closely align with the fundamental principles of a PEFA assessment, including the principles of evidence-based scoring and mandatory QA procedures

- Fiscal Transparency Evaluation (FTE). The PULSE framework considers the Fiscal Transparency Handbook (2018) and Fiscal Transparency Code, issued by the International Monetary Fund.

PULSE Characteristics

- It is a free "global good" and a user-friendly web-based self-assessment tool.

- Designed for national and subnational governments but may be also applied by any reporting entity, such as international organizations, central banks, public corporations, and other government agencies.

- Systematically collect information on the current performance of PSA systems, standards, and practices.

- As mentioned, offers one single tool to measure and report on both the conceptual and actual implementation of accrual accounting standards for the public sector

- Provide inputs for development of a comprehensive PSA reform strategy and roadmap

- Use the assessment’s results to develop policy recommendations and action planning to enable further strengthening of PSA systems and practices

-

The assessment methodology is based on

- The PEFA assessment framework.

- The latest set of IPSAS pronouncements, but also go beyond the IPSAS framework by assessing the current status of PSA systems and the state of reform.

- The quality of the assessment and the final report is ensured through multilayer QA arrangements, including an external validation process and the PULSE Check

PULSE Structure

The PULSE framework assesses six pillars of performance embracing a total of 30 indicators and 107 dimensions of a transparent, efficient, and effective PSA system. This assessment framework provides information useful for decision making and focuses on key measurable aspects of the PSA system. PULSE uses the results of the individual indicator calculations, which are based on available evidence, to provide an integrated assessment of the PSA system according to the six pillars of PSA performance.

Pilar I

Public Sector

Accounting

Framework

Pilar II

Financial

Assets &

Liabilities

Pilar III

Non-financial

assests and

liabilities

Pilar IV

Expense &

revenue

recognition

Pilar V

Financial

reporting &

consolidation

Pilar VI

Reform

prerequisites

and capacities

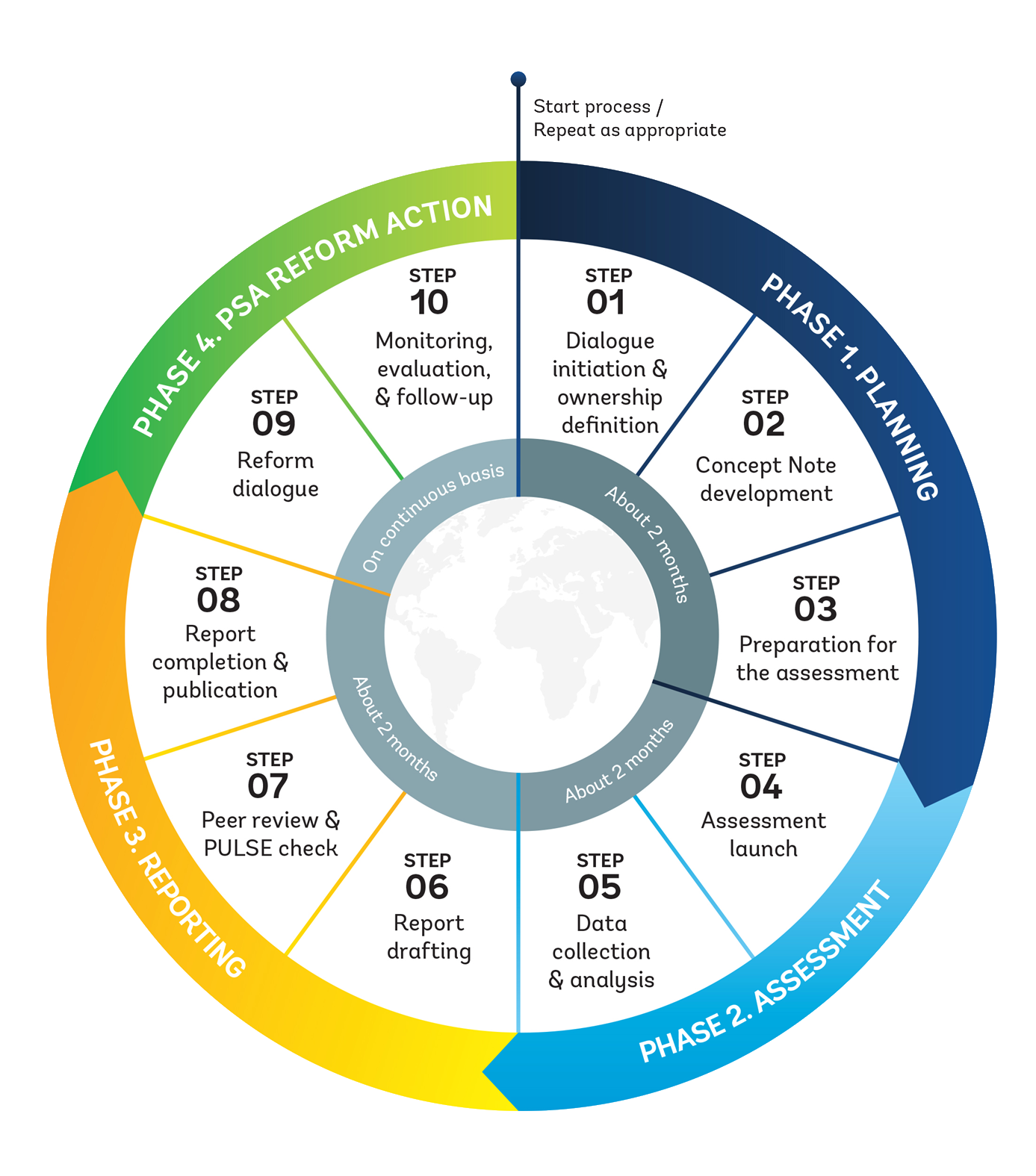

Assessment Process

Coverage

- PULSE recognizes that governments and other public sector entities are organized differently around the world – ministries, departments, secretaries, etc.

- The framework was designed to be usually conducted by national or subnational governments, but could also be used for other entities such as SOEs, central banks or other reporting entities.

- The coverage of consolidated entities – according to IPSAS definition - or subnational governments will depend on the local context and the number of controlled entities by the reporting entity.

Scope

- PULSE is usually based on the most recently completed fiscal year.

- The scope of each indicator may vary depending on the organizational structure of the reporting entity.

- It is imperative to clearly define the scope, based on the reporting entity that is being assessed, in the planning phase.

- During the assessment, information on aspects of defense, public order, and safety functions may in rare cases be unavailable for reasons of national security.

- Any limitations of this nature should be noted in the introduction of the report

Assessment modalities

- Full self-assessment approach, as a primary assessment mode. In this case, the PULSE is undertaken by the lead agency with mandatory external validation.

-

In exceptional cases, the following two modes are also possible:

- External assessment mode which is conducted by external experts; and

- Blended mode, which combines self-assessment with the assistance of external experts

- The option to choose these modes depends on the

jurisdictional situation , including resource availability and institutional capacity.

Pulse Reports

Armenia April 2024 - 3.8 Mb

Ukraine April 2024 - 3.0 Mb